All Categories

Featured

Table of Contents

They usually supply a quantity of coverage for a lot less than long-term types of life insurance policy. Like any kind of policy, term life insurance coverage has advantages and drawbacks relying on what will certainly work best for you. The advantages of term life include price and the ability to personalize your term size and coverage quantity based upon your requirements.

Depending on the type of policy, term life can supply fixed premiums for the entire term or life insurance policy on degree terms. The death benefits can be dealt with.

Proven Direct Term Life Insurance Meaning

You should consult your tax advisors for your particular factual scenario. Fees reflect plans in the Preferred Plus Price Class problems by American General 5 Stars My representative was extremely experienced and valuable in the procedure. No pressure to buy and the procedure fasted. July 13, 2023 5 Stars I was pleased that all my needs were satisfied without delay and professionally by all the representatives I spoke with.

All documentation was digitally finished with accessibility to downloading and install for personal documents upkeep. June 19, 2023 The endorsements/testimonials provided ought to not be understood as a referral to purchase, or an indication of the value of any services or product. The endorsements are actual Corebridge Direct consumers that are not affiliated with Corebridge Direct and were not provided compensation.

2 Cost of insurance policy rates are identified using methodologies that differ by business. It's vital to look at all elements when reviewing the general competition of prices and the value of life insurance policy coverage.

Tax-Free Direct Term Life Insurance Meaning

Like many group insurance policy policies, insurance policies provided by MetLife consist of certain exemptions, exemptions, waiting durations, reductions, constraints and terms for maintaining them in force (term 100 life insurance). Please contact your advantages manager or MetLife for costs and full details.

:max_bytes(150000):strip_icc()/Investopedia-terms-termlife-6451fde927474d4f8a81a5681efd393f.jpg)

For the most component, there are 2 types of life insurance intends - either term or long-term strategies or some combination of both. Life insurance companies offer numerous kinds of term strategies and standard life plans in addition to "rate of interest delicate" items which have actually come to be more common considering that the 1980's.

Term insurance supplies protection for a specified amount of time. This duration might be as brief as one year or provide coverage for a particular number of years such as 5, 10, 20 years or to a defined age such as 80 or in some cases as much as the earliest age in the life insurance policy death tables.

The Combination Of Whole Life And Term Insurance Is Referred To As A Family Income Policy

Presently term insurance rates are very competitive and amongst the most affordable traditionally skilled. It ought to be noted that it is a commonly held belief that term insurance coverage is the least costly pure life insurance policy protection readily available. One requires to examine the plan terms carefully to determine which term life options are appropriate to meet your particular scenarios.

With each new term the premium is enhanced. The right to renew the plan without proof of insurability is an essential benefit to you. Otherwise, the risk you take is that your health might deteriorate and you may be unable to acquire a policy at the exact same prices and even in all, leaving you and your beneficiaries without coverage.

You have to exercise this choice throughout the conversion period. The size of the conversion period will differ depending upon the sort of term policy purchased. If you transform within the recommended duration, you are not called for to offer any kind of details concerning your health. The premium rate you pay on conversion is normally based on your "existing achieved age", which is your age on the conversion day.

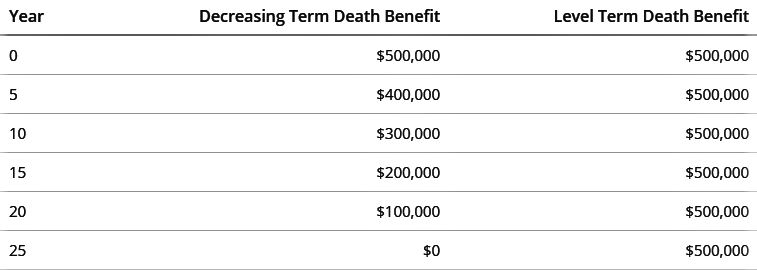

Under a degree term policy the face quantity of the plan stays the very same for the entire period. With decreasing term the face quantity decreases over the duration. The premium stays the exact same every year. Usually such plans are sold as mortgage defense with the quantity of insurance lowering as the balance of the home loan reduces.

Traditionally, insurers have not deserved to transform costs after the policy is offered (term 100 life insurance). Given that such plans may continue for several years, insurance firms should utilize conservative death, rate of interest and expenditure price estimates in the premium estimation. Adjustable premium insurance policy, however, enables insurance firms to provide insurance policy at lower "current" premiums based upon less conventional presumptions with the right to change these costs in the future

Comprehensive Direct Term Life Insurance Meaning

While term insurance coverage is created to supply protection for a defined time duration, long-term insurance is developed to offer protection for your whole lifetime. To maintain the costs price level, the costs at the more youthful ages goes beyond the actual cost of protection. This added premium develops a book (money worth) which helps spend for the plan in later years as the price of security surges over the costs.

The insurance policy business spends the excess premium dollars This kind of policy, which is often called money value life insurance policy, creates a cost savings element. Cash values are essential to a permanent life insurance plan.

Expert What Is Voluntary Term Life Insurance

Sometimes, there is no relationship in between the size of the money worth and the premiums paid. It is the cash money worth of the plan that can be accessed while the policyholder is active. The Commissioners 1980 Requirement Ordinary Mortality Table (CSO) is the present table used in determining minimal nonforfeiture values and policy reserves for normal life insurance policy plans.

Lots of permanent policies will certainly include stipulations, which specify these tax obligation requirements. There are two fundamental categories of permanent insurance coverage, conventional and interest-sensitive, each with a number of variations. Furthermore, each group is usually available in either fixed-dollar or variable type. Typical entire life plans are based upon long-lasting quotes of expenditure, passion and death.

If these estimates alter in later years, the company will change the premium accordingly yet never ever above the optimum ensured premium stated in the plan. An economatic entire life plan attends to a fundamental quantity of participating entire life insurance policy with an added supplementary coverage offered via the use of rewards.

Due to the fact that the costs are paid over a much shorter span of time, the costs repayments will be higher than under the entire life plan. Solitary premium entire life is limited repayment life where one huge exceptional settlement is made. The plan is totally paid up and no further premiums are needed.

{kind=link}

Latest Posts

Funeral Plan For Over 30

Senior Solutions Final Expense

Best Funeral Insurance Companies